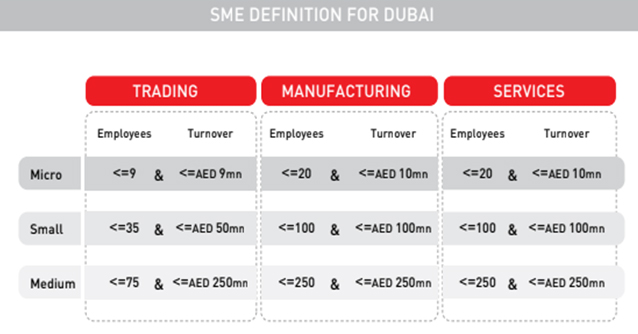

An enterprise engaged in an economic activity

An enterprise which meets the thresholds of Employee Headcount and (Annual) Turnover

Primary Industries: Trading / Manufacturing / Services

- Micro

- Small

- Medium

Further nuances – Independence criteria

Because SMEs can be linked or have a stake in another enterprise regardless if it is large or an SME as well.

Classifications:

- Autonomous Enterprise

- Partner Enterprise

- Linked Enterprise

WHY DEFINE SMEs ?

An established definition let’s all stakeholders be on the same page, and can be used as a starting point for any initiative / measure / audit of any endeavor to be undertaken for the sake of developing SME competitiveness and its support system.

How was this definition formulated?

- Macroeconomic data – GDP Contribution, employment and trade flows were evaluated to ensure that the definition is in line with the economic reality in Dubai.

- Pegged with international and regional definitions

- Assessment of the business philosophies, perspectives and application of the SMEs definition across key stakeholders including free economic zones, banks and relevant government entities.

- Thresholds were developed by assessing the typical SME landscape/structures in various countries.

SECTION I. Economic Assessment

The Dubai Economy

- Dubai’s economic amounted to no less than 10% between 2000 to 2012.

- Diversification of the economy has been the priority during this time.

- The Global Financial Crisis impacted Dubai by shaving 2.4% off its GDP.

- But its robust growth in the past years laid the groundwork for it to bounce back in 2010 with a 2.8% growth for that year.

- Foreign trade has been key to this growth with a peak of 753 million AED in 2011 (76% of the UAE’s overall trade for that year).

- Trade and Services sector remain robust contributor to Dubai’s economy.

- Services sector contribute to the 57% of Dubai’s GDP during 2009-2012.

Notable contributors to the Service Sector:

Construction – 9%

Real Estate Industry – 14%

Transport, Storage and Communications – 14%

Hotels and Restaurants – 3.9%

Business and SME Landscape

SMEs account for 95% of establishments in Dubai

Micro firms – 72%

Small firms – 18%

Medium firms – 5%

Breakdown of SMEs located in Dubai between major sectors:

Trading Sector – 57% Services Sector – 35%

Manufacturing – 8% Over 16,600

Business Licenses were issued in 2012

Commercial Licenses alone amount to 75% of the licenses issued in 2012

Followed by Professional Licenses at 23%

COMPOSITION OF KEY SECTORS

1. Manufacturing

Breakdown according to business:

Wearing apparel (clothes) – 33%

Fabricated metal products (except machinery and equipment) – 16%

Remaining 51% unspecified

Manufacturing – Breakdown according to employee composition:

54% of Manufacturing firms have 1 – 10 employees

20% of Manufacturing firms have 11 – 25 employees

Remaining 26% unspecified

Manufacturing Licenses issued between 2009 to 2012:

Food & Beverage Manufacturing – 24% with an annual growth of 12%

Basic & Fabricated Metal Manufacturing – 21%

2. Services

Services – Breakdown according to business:

Real Estate, Renting and Business Services – 33%

Construction & Contracting Firms – 27%

Transportation and Telecommunications – 17%

Hotels and Restaurants – 10%

Services – Breakdown according to employee composition:

Real Estate, Renting & Business Services – 38%

Construction & Contracting – 31%

3. Trading

Key sectors:

Consumer Goods

Textiles and Textiles & Garments Trading

IT and Telecom Products

General Trading

No Industry share specified

Trading – Breakdown according to employee composition:

89% of Trading firms have 1 – 10 employees

9% of Trading firms have 11 – 25 employees

Trading Licenses issued between 2009 to 2012:

Consumer Goods Trading – 25%

Textiles and Garments – 16%

Remaining businesses not specified

SECTION II. Performance of Dubai’s SME Sector

Economic Performance

Gross value added – metric used to measure the difference between output and intermediate consumption.

SMEs contribute around 40% to total value add generated by Dubai’s Economy

Micro – 8%

Small – 14%

Medium – 17%

Gross Value Added Contribution based from SME Sector:

Trading SME – 47%Service SME – 41%

Manufacturing – 13%

SME hold 42% share of the total workforce in Dubai

SME employment share based on Size:

Micro – 14.6%

Small – 16.4%

Medium – 11%

SME employment share based on Sector:

Services – 51%

Trading – 33%

Manufacturing – 16%

Business Performance

SME Productivity per unit (gross value-add) by Size:

Medium – AED 244,785

Small – AED 138,058

Micro – AED 91,080

SME Productivity per unit (gross value-add) by Sector:

Trading – AED 210,447

Manufacturing – AED 122,255

Service – AED 118,480

Overall, SME productivity is still lower compared to large businesses within Dubai and its similarly sized counterparts in other countries.

Key reasons for this observation:

- Low focus of businesses in improvements / re-engineering of business processes to improve efficiency

- Limited focus on businesses on training, development and up skilling of employees due to the transient nature of the workforce

- Limited adoption by businesses of advanced enterprise level ICT systems (such as ERP, CRM solutions)

SECTION III. Financial Health of Dubai’s SMEs

Dubai SMEs tend to maintain sufficient short-term assets to cover their short-term liabilities

Manufacturing SMEs operate in the safest threshold

Trading SMEs are more at long-term risk due to accumulation of receivables and inventory

Service SMEs are also at long-term risk due to accumulation of receivables

Cash Conversion Cycle per SME Sector:

Service – 25 to 60 days

Manufacturing – 30 to 60 days

Trading – 40 to 85 days due to the following:

-Lower stock turnover ratio

-High proportion of sales on credit

-Lesser number of purchase outstanding days

SECTION IV. State and Characteristics of Dubai’s SMEs

Study done with a sample size of 500 SMEs across Manufacturing, Trading and Services.

Degree of International Orientation

- Dubai SMEs are highly export-oriented – 51% indicated they have revenue coming in from regional and international markets.

- Trading SMEs are inherently more

export-oriented.

- 68% of Trading SMEs are involved in international markets

- 53% of Manufacturing SMEs are involved in international markets

- 37% of Service SMEs are involved in international markets

- Medium SMEs have the highest export market involvement

- 66% of Medium enterprises indicate they have revenues coming from international markets

- 55% of Small enterprises indicate they have revenues coming from international markets

- 39% of Micro enterprises indicate they have revenues coming from international markets

- GCC, Asia-Pacific and Africa are the biggest markets Dubai SMEs export their products and services to.

- Overall degree of International Orientation: HIGH

- Sector with Highest Orientation: TRADING

Prevalence of Innovation

- Only 8% of survey respondents indicate they maintain an annual budget for Research and Development

- Only 13% of survey respondents indicated they have implemented some level of innovation in either their products or enhancements to their processes

- Prevalence of innovation among

respondents are divided in the following business aspects:

- Products/Services – 42%

- International Processes – 30%

- Distribution/Delivery Formats – 28%

- Majority of respondents indicate they pursue innovation where they perceive they’ll gain a competitive advantage.

- Prevalence of innovation by SME

Sector:

- Manufacturing – 29%

- Services – 16%

- Trading – 4%

- As expected, the smaller the enterprise is, the less it is inclined to innovate.

- It is observed that more internationally oriented SMEs give more attention to innovating relevant business lines.

- Overall Degree of Innovation Orientation: LOW

- Sector with Highest Orientation: MANUFACTURING

Level of IT Adoption

- 21% of total survey respondents indicate they use advanced IT systems (ERP and CRM system)

- Service firms lead the Dubai SME Sectors in adopting IT systems:

- Services – 26%

- Manufacturing – 18%

- Trading – 16%

- 29% of SMEs have dedicated IT employees/departments

- SMEs involved in exporting have a high ratio of IT adoption versus non-exporters across all sectors and enterprise sizes.

- Overall degree of IT adoption: MODERATE

- Sector with the Highest Orientation: SERVICES

Degree of Human Capital Development Orientation

- Indicates the amount of management focus and company resources allocated to employees

- 25% of survey respondents indicate they have a dedicated Human Resource department

- 72% of respondents indicate they evaluate and reward their employees’ performance on a regular basis

- Service SMEs lead the pack in

terms of human capital development:

- 30% of Service SMEs indicate they conduct regular performance appraisals

- 32% of Service SMEs indicate they provide comprehensive OR need-based training to their employees

- Key reason: Service SMEs are more reliant on human resources; where business success is reliant on the quality and performance of the human resource

- Data for other sectors not indicated

- There is a trend of increase human

capital development as the enterprise grows larger.

- However, the scale by which this develops is dependent on the sector the enterprise belongs to.

- Overall degree of Human Capital Development Orientation: Moderate

- Sector with the Highest Orientation: Services

Degree of Corporate Governance

- Indicates the level of formalization of the organizational structure

- Quality of financial reporting mechanisms

- Adherence to corporate governance

principles

- E.g. Advisory board, strategic planning, framework management and documented policies

- 34% of respondents indicate they have a formal organizational structure

- 50% indicated they maintain audited financial statements

- Only 18% of respondents indicate they adhere to corporate governance principles

- Orientation towards corporate

governance is directly proportional to enterprise size:

- 42% of Medium enterprises indicate they adhere to one or more corporate governance principle

- 20% of Small enterprises indicate they adhere to one or more corporate governance principle

- Only 4% of Micro enterprises indicate they adhere to one or more corporate governance principle

- Adoption of corporate governance

principles by sector:

- Manufacturing – 26%

- Service – 18%

- Trading – 14%

- Key corporate governance

principles being adhere to by Dubai SMEs:

- 13% of respondents have formal mechanism for financial planning and management reporting

- 11% of respondents have independent board of directors

- 11% of respondents indicate they have documented policies and procedures for key processes

- Overall degree of Corporate Governance Orientation: LOW

- Sector with the Highest Corporate Governance Orientation: MANUFACTURING

Levels of Access to Finance

- Defined as access to finance for capital require to start the business

- Defined as access to finance for business operations and expansion

- Type of bank financing access

- Key finding: There is a limited

availability of externally sourced financing for SMEs in Dubai

- 80% of survey respondents indicated using personal money/savings as the primary source of capital

- Availability of bank finance for growth and operation is also limited with only 23% of respondents indicating they availed of financial products from banks in the last 5 years

- Long-term financing requirements of SMEs are found within the range of 1 million to 5 million AED. While short term financing requires an annual 1 million AED.

- Access to bank finance is more prevalent within Trading SMEs.

- Access to bank finance is more prevalent with Medium SMEs.

- Overall state of Finance: MODERATE

- Sector with the Highest Access to Finance: TRADING

Scalability Potential

- Defined as the current capacity of

enterprises to fully utilize business assets and resources

- E.g. equipment and human resources

- Share of fixed operating costs vis-a-vis total operational cost.

- Expectation of annual growth in

demand of products/services in the market over the medium range (3-5 years)

- High growth expectation – 10%

- Medium growth expectation 5-9%

- Low growth expectation – X < 5%

- 70% of SMEs expect medium to high growth in demand for their good and services over the medium term.

- 45% of SMEs surveyed indicate their capacity utilization is higher than 75%

- Trading SMEs tend to have low

fixed cost structure.

- 46% of Trading enterprises indicate their fixed cost overhead only goes up to 30% of their total cost.

- Survey reflect 19% of SMEs in

Dubai – across all sectors – have high scalability potential:

- Scalability in Manufacturing – 21%

- Scalability in Trading – 20%

- Scalability in Services – 17%

- Overall Scalability: LOW

- Sector with Highest Scalability: Marginal difference between sectors.

SECTION V. Business Outlook of Dubai’s SMEs

- Despite mixed scores, the Business Confidence Index calculates that Dubai’s SME segment stands at 119.5 points, reflecting an overall positive business outlook with a confidence in continued growth.

- Key Business Objectives of SME Respondents:

- Expansion into new regional markets

- Increasing revenue for existing businesses

SECTION VI. Government Support Ecosystem for SMEs

- The UAE Government is giving high focus on enhancing the contribution and performance of the SME segment of its economy. A number of policies have been implemented to set the groundwork for both direct and indirect government support.

- The Dubai SME is a key government entity in the promotion and growth of SMEs in Dubai.

- Policy-level Programs

- Start-up Subsidies

- Government Procurement Program

- Support Programs and Services by the Dubai SME

- Development Advisory

- Capability Development

- Business Incubation

- Entrepreneur Relations

- Funding Support

- Outreach Initiatives

- Young Entrepreneur Competition

- Mohammed Bin Rashid Award for Young Business Leaders

- SME Development Programs

- Dubai SME100

- Corporate Governance for SMEs

- SME Bank Friendliness Index

- Be-Bankable

- The UAE Government, together with the Dubai SME Agency is adopting a holistic approach in promoting entrepreneurship and growth of the SME sector in Dubai

One Reply to What are the impact of SMEs and why they matter in the UAE?

Great content! Super high-quality! Keep it up! 🙂

7 Cloud POS Software Myths and Why They Are False